DSCR

Start maximizing your real estate investment potential.

Focus on the property's cash flow

Flexible and accessible option for investors

Find the right financing solution for your investment goals

888-549-1005

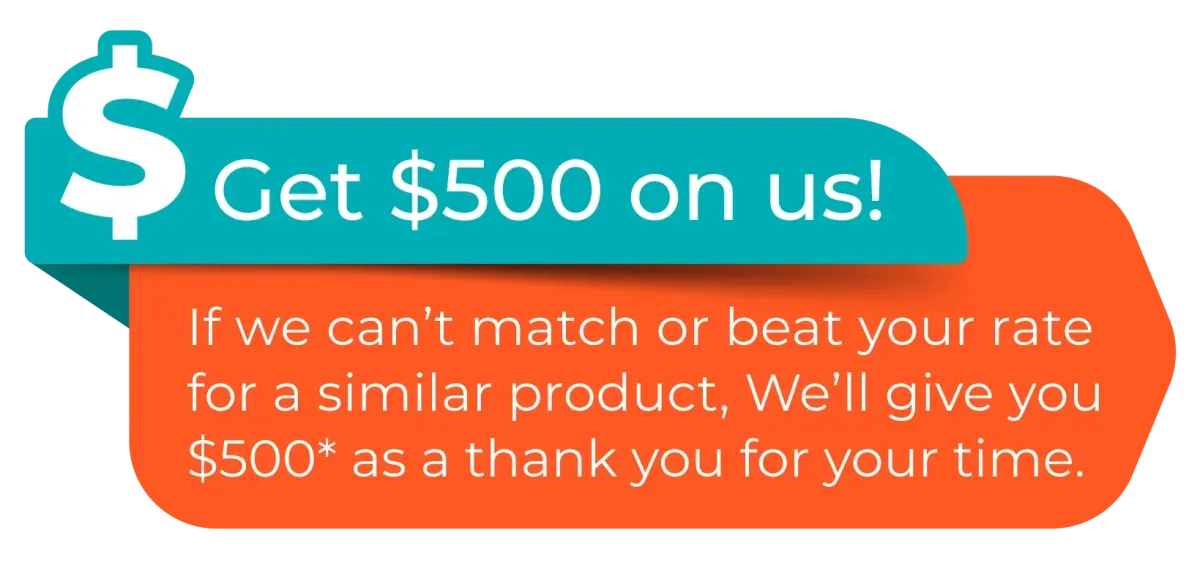

Call for a Free Mortgage Saving Report

No Credit Checks Required

Find Your Perfect Mortgage Match – Let’s Get Started!

DSCR

Or Get a Free Rate Quote

1800-725-9946

Start maximizing your real estate investment potential.

Focus on the property's cash flow

Flexible and accessible option for investors

Find the right financing solution for your investment goals

888-549-1005

Call for a Free Mortgage Saving Report

No Credit Checks Required

Get Approved for a DSCR Loan — Easy Financing for Real Estate Investors Without Income Verification!

No Personal Income Verification Needed: — Approval based on the property’s cash flow, not your income or tax returns.

Perfect for Real Estate Investors: — Grow your rental portfolio with fast and flexible financing.

Competitive Interest Rates: — We secure the best possible rates to maximize your rental income and ROI.

Fast Pre-Approval Process: — Move quickly on investment properties with our streamlined approval.

Flexible Loan Programs: — Designed to fit your investment strategy and long-term goals.

Low Closing Costs & No Hidden Fees: — Full transparency to help you keep more of your profits.

Find Your Perfect Mortgage Match – Let’s Get Started!

Start with our Mortgage Approval Tool!

Start with our Mortgage Approval Tool!

Home Purchase

Ready to buy? Get pre-approved in minutes and secure competitive rates tailored to your budget. Whether you’re a first-time buyer or upgrading, we’ll help you close faster.

Home Refinance

Slash your monthly payments or tap into your equity with flexible refinancing options. Rate-and-term, cash-out, or FHA streamline—we’ve got your best deal.

Home Equity

Need funds for renovations, debt consolidation, or emergencies? Access up to 90% of your home’s value with low rates and tax-deductible interest

Reverse

Age 62+? Keep ownership, stay in your home, and access tax-free cash. No monthly payments required—ever. FHA-insured and risk-free.

🏡What Is an DSCR Loan in Geogia? | Requirements & Benefits

Affordable home financing designed to help more Georgian buy a home.

A DSCR loan in Georgia is a mortgage program designed specifically for real estate investors purchasing or refinancing rental properties. DSCR stands for Debt Service Coverage Ratio, which measures whether the rental income generated by a property is sufficient to cover the mortgage payment.

Unlike traditional mortgage loans that rely heavily on personal income verification, DSCR loans focus primarily on property cash flow and rental income performance. This makes DSCR financing a popular solution for investors who want to scale their rental portfolios without the limitations of traditional mortgage qualification methods.

DSCR loans are commonly used throughout Georgia in cities such as Atlanta, Savannah, Augusta, Columbus, Macon, and Athens, where strong rental demand continues to attract real estate investors.

Start with our Mortgage Approval Tool!

Our Service Commitment

No Hidden Fees: We believe in clear and upfront communication about all costs associated with your mortgage.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Get Expert Advise, every time from a licensed loan officer with a suite of products to choose from.

Our Team strives to deliver excellence, reach us day or night about any of your mortgage questions, we’re here for you when you need.

Working with us or just thinking of it, we will always be honest and transparent. No sales targets means way better service!

DSCR Loan Requirements Georgia

To qualify for a DSCR loan in Georgia, borrowers must meet certain financial and property guidelines established by lenders.

Basic DSCR Loan Requirements

Property must be used as an investment or rental property

Rental income must support the mortgage payment

Minimum credit score requirements

Down payment or property equity requirements

Property appraisal confirming rental market value

Acceptable debt service coverage ratio (DSCR)

Many DSCR loan programs do not require traditional income documentation such as tax returns or employment verification.

Your Trusted Georgia Partner for DSCR Home Financing

Qualifying for a DSCR mortgage focuses primarily on the cash flow potential of the investment property rather than the borrower’s personal income.

Flexible approval guidelines • Lower down payment options

How to Qualify for DSCR Loan in Georgia

Steps to Qualify

Apply for mortgage pre-approval

Provide property details and estimated rental income

Property appraisal confirming rental market value

DSCR ratio evaluation by the lender

Credit review and underwriting

Final loan approval and closing

DSCR Mortgage Georgia for Real Estate Investors

DSCR loans are specifically designed to help real estate investors finance rental properties without traditional income verification requirements.

Why Investors Choose DSCR Loans

Qualification based on rental income rather than employment income

Ability to finance multiple investment properties

Flexible financing for real estate portfolios

Efficient scaling of rental property investments

Long-term financing solutions for investors

Investors commonly use DSCR loans for single-family rental homes, small multifamily properties, and short-term rental investments.

DSCR Loan Minimum Credit Score Georgia

Credit score requirements for DSCR loans vary depending on the lender and loan program.

Typical Credit Score Guidelines

Many DSCR programs require minimum scores around 620–680

Higher credit scores may qualify for better loan terms

Strong credit profiles may receive lower interest rates

Credit score is evaluated alongside property cash flow and overall loan structure.

DSCR Loan Pre-Approval Georgia

Mortgage pre-approval is an important first step for investors planning to finance rental properties using DSCR loans.

Key benefits of a Texas rural development loan include:Benefits of DSCR Pre-Approval

Determines investment purchasing power

Confirms credit eligibility

Strengthens offers when purchasing investment properties

Helps accelerate loan closing timelines

Pre-approved investors can move quickly when attractive property opportunities arise.

DSCR Loan Pre-Approval Georgia

Mortgage pre-approval is an important first step for investors planning to finance rental properties using DSCR loans.

Key benefits of a Texas rural development loan include:Benefits of DSCR Pre-Approval

Determines investment purchasing power

Confirms credit eligibility

Strengthens offers when purchasing investment properties

Helps accelerate loan closing timelines

Pre-approved investors can move quickly when attractive property opportunities arise.

Start Your DSCR Loan in Georgia

For investors looking to expand their rental property portfolios, DSCR loans provide a flexible financing solution focused on property performance rather than personal income documentation.

Obtaining DSCR mortgage pre-approval helps investors evaluate property opportunities and move forward with confidence.

Our Service Commitment

Get Expert Advice every time from a licensed loan officer with a suite of products to choose from.

Our team strives to deliver excellence. Contact us day or night with any mortgage questions—we’re here when you need us.

Working with us or just thinking of it, we will always be honest and transparent. No sales targets means way better service!

No Hidden Fees: We believe in clear and upfront communication about all costs associated with your mortgage.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Available When & Where

You Want!

Across multiple states, our licensed loan officers will help you from application to funding and beyond.

We work on your schedule. With streamlined technology and dedicated support staffing, your mortgage request is always our priority!

Your Trusted Texas Partner for FHA Home Financing

FHA loans offer a reliable path to homeownership, specifically designed to help first-time buyers and those with lower credit scores secure affordable, stress-free financing.

Flexible approval guidelines • Lower down payment options

How to Qualify for an FHA Loan in Texas

Step-by-Step FHA Qualification Process

Mortgage pre-approval

Income and employment verification

Credit review

Debt-to-income calculation

Home appraisal

Underwriting approval

Final loan closing

Largest Lender Network in Florida, Georgia & Texas

Available When & Where You Want!

Across multiple states our Licensed Loan officers will help you from the application to the funding and beyond.

We work on your schedule, with streamlined technology and support staffing, your mortgage request will always be a priority!

Book an Appointment

Book an Appointment

See What Our Clients Say About Us!

Meet Our Team

Angle Ogbele

Natasha Staplowski

Darnell Smith

Arlan Zuberi

Meet Our Team

Angle Ogbele

Natasha Staplowski

Darnell Smith

Arlan Zuberi

What is DSCR?

A Debt Service Coverage Ratio (DSCR) loan is a type of commercial real estate loan where the lender evaluates the cash flow of the income-generating property to determine the borrower's ability to repay the loan. Instead of focusing primarily on the personal income and credit history of the borrower, the DSCR loan looks at the expected income the property will produce and whether it will be sufficient to cover the loan payments.

The DSCR is calculated by dividing the property's annual net operating income by the annual mortgage debt service (principal and interest payments). For example, if a property generates $120,000 in net operating income annually and the annual mortgage debt service is $100,000, the DSCR would be 1.2 ($120,000 / $100,000 = 1.2).

How Does DSCR Works?

Sufficient DSCR: The primary requirement is that the property's net operating income (NOI) must cover the mortgage debt service by a certain ratio. Lenders usually look for a DSCR of 1.20x or higher, meaning the NOI should be at least 20% greater than the debt service.

Property Appraisal: The lender will require an appraisal to determine the property's value and its capacity to generate income.

Down Payment: A larger down payment is often required for DSCR loans compared to traditional residential mortgages. This could be anywhere from 20-30% or more, depending on the lender's criteria.

Credit Score: While the property's income is the focus, a good credit score can still be important. Some lenders may have minimum credit score requirements, though these can be more flexible than for traditional loans.

Reserves: Lenders may require the borrower to have a certain amount of cash reserves on hand to cover potential vacancies or maintenance issues.

Property Type: DSCR loans can be used for various types of properties, including single-family rentals, multi-family dwellings, mixed-use buildings, and commercial properties. The lender will assess the property type and its income-generating potential.

Loan-to-Value (LTV) Ratio: The LTV ratio is another factor lenders consider. A lower LTV means more equity in the property and can be a favorable point in qualifying for a DSCR loan.

Business Plan: For commercial properties, a lender may require a solid business plan that shows how the property will generate income.

Experience: Some lenders may prefer borrowers with experience in managing rental or commercial properties, although this is not always a requirement.

Legal and Compliance Checks: As with any loan, there will be a need to ensure that the property complies with local zoning and building codes and that there are no legal encumbrances that would impact the lender's security interest in the property.

Each lender may have their own specific requirements and underwriting criteria, so it's important to check with potential lenders to understand their particular process for obtaining a DSCR loan.

Benefits of DSCR

Income-Based Lending: The loan approval is based on the cash flow generated by the property, not the personal income of the borrower.

Minimal Emphasis on Personal Finances: Personal income verification is often not required, and the borrower's credit score may have less impact on the loan decision than with traditional loans.

Property as Collateral: The loan is secured by the commercial property, and the lender focuses on the property's ability to generate sufficient income to cover the debt payments.

DSCR Calculation: Lenders calculate DSCR by dividing the property's Net Operating Income (NOI) by the annual debt obligations. A DSCR of 1.0 means the NOI is equal to the debt service, while lenders look for a DSCR greater than 1.20.

Flexible Loan Terms: DSCR loans may offer a variety of terms, including fixed or adjustable interest rates and different amortization schedules.

Higher Interest Rates: Interest rates for DSCR loans may be higher than traditional commercial loans due to the perceived higher risk associated with not considering the borrower's personal income.

Larger Down Payment: Borrowers often need to make a larger down payment, sometimes 25-30% or more, depending on the lender's requirements and the property's cash flow.

Prepayment Penalties: There may be prepayment penalties, especially if the loan has a fixed rate, as lenders expect a certain return on their investment.

Non-Recourse Financing: Some DSCR loans may be non-recourse, meaning the lender's recovery in the event of default is limited to the property itself, without going after the borrower's other assets.

Loan Size and Term: DSCR loans can vary in size and term, potentially offering more flexibility than traditional commercial loans depending on the lender and the property in question.

Features of DSCR

Focus on Property Income: The main criterion for a DSCR loan is the income generated by the property, which means personal income and credit history are less scrutinized. This can be advantageous for investors who have complex financial situations or fluctuating personal incomes.

Potential for No Income Verification: Since the loan is underwritten based on the property's cash flow, there may be no need for traditional income verification, which can simplify the application process for self-employed individuals or those with non-traditional income sources.

Higher Loan Amounts: DSCR loans can offer access to financing for more expensive properties that exceed conventional loan limits, which can be particularly useful in high-cost real estate markets.3

Flexibility for Multiple Properties: Investors with multiple properties can benefit from DSCR loans, as they allow for the consideration of each property on its own merits, rather than aggregating the debt across all properties owned by the borrower.

Non-Recourse Options: Some DSCR loans may be non-recourse, which means the lender's recovery in the event of default is limited to the property itself, and personal assets are not at risk.

Interest-Only Payment Options: Certain DSCR loans may offer interest-only payment periods, which can reduce the monthly payment amount and improve short-term cash flow for the borrower.

Longer Amortization Periods: These loans can have longer amortization periods, which can lower the monthly payments and make it easier to manage cash flow.

Potential Tax Benefits: The interest on the mortgage may be tax-deductible, and investors can also potentially benefit from depreciation and other real estate-related deductions.

Asset-Based Lending: For investors looking to grow their portfolios without being limited by their personal debt-to-income ratio, DSCR loans provide an opportunity to leverage the property's income potential.

Streamlined Financing for Investors: Investors looking to quickly close on a property may find that DSCR loans can offer a more streamlined process compared to traditional loans, especially if they have a strong DSCR ratio and the property is in good condition.

#1 Voted Mortgage Calculators in Canada

Our Mortgage Experts

Dylan James

Mortgage Agent Level 1

Abdoulaye Sow

Mortgage Agent Level 1

Michael Le Chi

Mortgage Agent Level 1

Heith Gharib

Mortgage Agent Level 1

Sara Fresco

Mortgage Agent level 1

Mortgage Learning Center

No blogs found

Quick Links

Other Links

Contact Information

RateShop Mortgage LLC is a licensed mortgage broker in FL and TX.

In accordance with federal law, we do not engage in business practices that discriminate on the basis of race, color, religion, national origin, sex, marital status, or age (provided you have the capacity to enter into a binding contract), nor do we discriminate because any part of your income is derived from public assistance programs, or because you have, in good faith, exercised any right under the Consumer Credit Protection Act. The Federal Trade Commission, Equal Credit Opportunity Division, Washington, DC 20580, is the federal agency responsible for administering these laws.

TEXAS RESIDENTS: CONSUMERS WISHING TO FILE A COMPLAINT AGAINST A MORTGAGE COMPANY OR RESIDENTIAL MORTGAGE LOAN ORIGINATOR LICENSED IN TEXAS SHOULD SEND A COMPLETED COMPLAINT FORM TO THE DEPARTMENT OF SAVINGS AND MORTGAGE LENDING (SML): 2601 N. LAMAR BLVD., SUITE 201, AUSTIN, TEXAS 78705

TEL: 1-877-276-5550. INFORMATION AND FORMS ARE AVAILABLE ON SML'S WEBSITE: SML.TEXAS.GOV.

Copyright 2026. All Rights Reserved Rateshop Mortgage LLC