Residential

Construction

Loans

Get Flexible Financing for Your Custom Home Project

Loans for major renovations or new construction

Competitive rates and flexible terms

Funds disbursed in stages based on project completion

888-549-1005

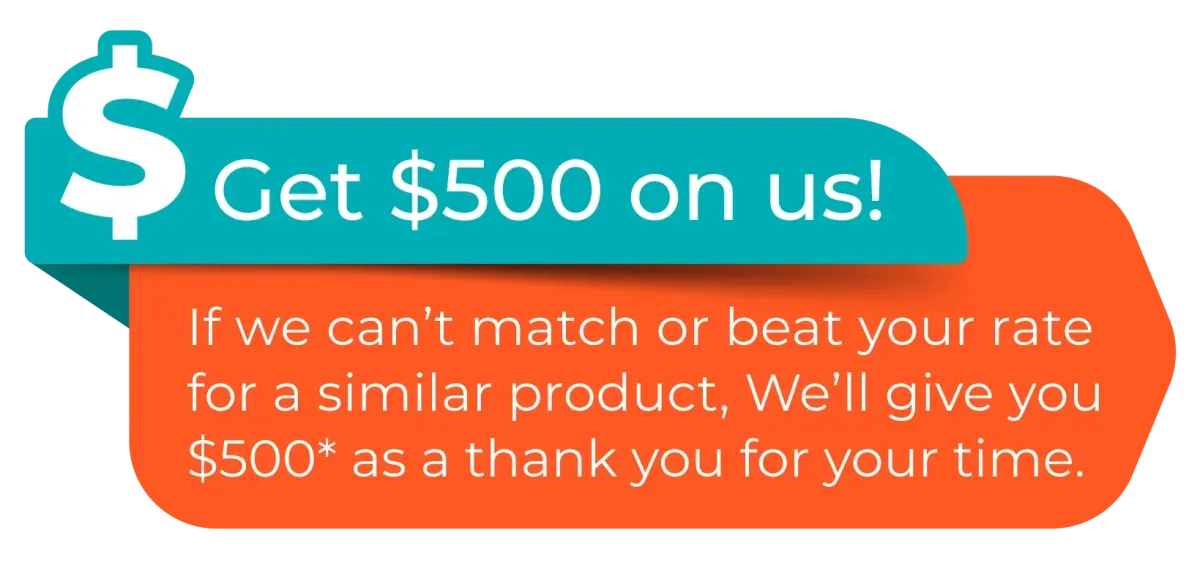

Call for a Free Mortgage Saving Report

No Credit Checks Required

Find Your Perfect Mortgage Match – Let’s Get Started!

FHA Loans

FHA Loans

Or Get a Free Rate Quote

1800-725-9946

Make your dream of owning a home a reality.

Low down payment options

Flexible credit requirements

Competitive interest rates we shop for you

888-549-1005

Call for a Free Mortgage Saving Report

No Credit Checks Required

Residential Construction

Loans

Or Get a Free Rate Quote

1800-725-9946

Get Flexible Financing for Your Custom Home Project

Low down payment options

Flexible credit requirements

Competitive interest rates we shop for you

888-549-1005

Call for a Free Mortgage Saving Report

No Credit Checks Required

Start with our Mortgage Approval Tool!

Build Your Dream Home with Our Residential Construction Loans — Fast Approvals, Flexible Terms, and Expert Support!

Flexible Financing for New Construction: — Fund your custom home build from start to finish with ease.

Interest-Only Payments During Construction: — Lower payments while your home is being built.

Fast Pre-Approval to Get Your Project Started: — Move forward quickly and break ground without delays.

Competitive Interest Rates: — We help secure the best rates to keep your project affordable.

Expert Guidance Every Step of the Way: — Our team handles the process and works directly with your builder.

One-Time Close Options Available: — Combine construction and permanent financing to save time and money.

Find Your Perfect Mortgage Match – Let’s Get Started!

Start with our Mortgage Approval Tool!

Home Purchase

Ready to buy? Get pre-approved in minutes and secure competitive rates tailored to your budget. Whether you’re a first-time buyer or upgrading, we’ll help you close faster.

Home Refinance

Slash your monthly payments or tap into your equity with flexible refinancing options. Rate-and-term, cash-out, or FHA streamline—we’ve got your best deal.

Home Equity

Need funds for renovations, debt consolidation, or emergencies? Access up to 90% of your home’s value with low rates and tax-deductible interest

Reverse

Age 62+? Keep ownership, stay in your home, and access tax-free cash. No monthly payments required—ever. FHA-insured and risk-free.

Start with our Mortgage Approval Tool!

Our Service Commitment

No Hidden Fees: We believe in clear and upfront communication about all costs associated with your mortgage.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Get Expert Advise, every time from a licensed loan officer with a suite of products to choose from.

Our Team strives to deliver excellence, reach us day or night about any of your mortgage questions, we’re here for you when you need.

Working with us or just thinking of it, we will always be honest and transparent. No sales targets means way better service!

Largest Lender Network in Florida, Georgia & Texas

What Are Residential Construction Loans?

A residential construction loan is a short-term financing option designed for individuals or builders in the United States looking to construct a new home or undertake significant renovations on an existing property. Unlike a traditional mortgage that is based on the value of a completed house, a residential construction loan is used to cover the costs of building a home from the ground up or completing major remodeling projects.

How Does a Residential Construction Loans Works?

Loan Limits

Residential construction loans are tailored to finance the building of a new home, with limits determined by the estimated construction costs and the projected market value upon completion. Lenders use these criteria to ensure the project is both feasible and financially sound.

Interest Rates

Interest rates on construction loans tend to be higher than those on permanent mortgages due to the elevated risk during the construction phase. Typically, these rates are adjustable during construction and may convert to fixed rates once the project is completed and the loan transitions to permanent financing.

Down Payment

Borrowers are generally required to make a substantial down payment—often 20% or more of the total construction cost—to secure a residential construction loan. This upfront investment demonstrates financial commitment and helps mitigate the lender's risk during the building process.

Credit Score

A strong credit score is essential when applying for a construction loan, as lenders typically look for scores of 700 or above. A high credit rating indicates reliable credit management and increases the likelihood of receiving favorable loan terms.

Debt-to-Income Ratio

Lenders carefully evaluate your debt-to-income (DTI) ratio to ensure you can manage both existing obligations and the additional costs associated with building a home. A DTI below 43% is generally preferred, underscoring a healthy balance between income and debt levels.

Cash Reserves

Robust cash reserves are a critical requirement for construction loans, as they provide a financial buffer against potential delays or unforeseen construction costs. Lenders often mandate that borrowers have enough reserves to cover several months of mortgage payments.

Documentation

Applying for a residential construction loan involves extensive documentation. Applicants must provide detailed construction plans, budgets, tax returns, bank statements, and other financial records, allowing lenders to thoroughly assess the project's viability and the borrower's repayment capability.

Appraisal

A comprehensive appraisal is conducted to estimate the future value of the property once construction is complete. This appraisal plays a key role in determining the maximum loan amount, ensuring that the funds provided align with the projected market value and overall scope of the project.

Features of Residential Construction Loans

Customization

It allows you to build a custom home tailored to your specific needs, preferences, and lifestyle, rather than settling for a pre-existing home that may not meet all your requirements.

Control Over Construction

You have more control over the construction process, including the selection of materials, finishes, and fixtures, ensuring the final product is exactly what you want.

Incremental Funding

The loan provides funds in stages as construction progresses, which helps manage cash flow and ensures that builders are paid on time for completed work.

Interest-Only Payments

During the construction phase, you only pay interest on the funds that have been disbursed, not the entire loan amount, which can help keep initial expenses lower.

One-Time Closing

Some construction loans offer a one-time closing, which means you only go through the loan application and closing process once. After construction, the loan automatically converts to a permanent mortgage without the need for a second closing.

Potential Equity Growth

If the construction project is managed well and the final property value exceeds the cost of construction, you may benefit from immediate equity in the new home.

Brand New Home

Upon completion, you'll have a brand-new home that should require less maintenance and fewer repairs in the early years compared to an older home.

Energy Efficiency

New homes can be built with the latest energy-efficient technologies and materials, potentially reducing utility costs and offering a more sustainable living environment.

Overall, a residential construction loan can be an excellent financial product for building your dream home, giving you the financial flexibility to fund the construction process while potentially adding value to your investment from the start.

Benefits of Residential Construction Loans

Short-term Financing

Construction loans are short-term loans, with a duration of one year or until the construction of the home is complete.

Interest-Only Payments

During the construction phase, borrowers usually make interest-only payments on the money that has been disbursed to date.

Draw Schedule

Funds are released in a series of draws as construction milestones are completed, rather than a single lump sum at the beginning of the loan.

Variable Rates

The interest rates on construction loans are often variable, which means they can fluctuate with the market during the construction period.

Rigorous Approval Process

Lenders require detailed construction plans, a qualified builder, a detailed budget, and sometimes a down payment.

Builder Approval

The builder or contractor must often be approved by the lender to ensure that they have the necessary qualifications and financial stability to complete the project.

Inspections

The lender will conduct periodic inspections to verify that the construction is progressing as planned before releasing subsequent draws.

Convertibility

Many construction loans are designed to convert to a traditional mortgage after the completion of the home, known as a 'construction-to-permanent' loan.

Down Payment

Borrowers often need to make a significant down payment, which can range from 10% to 20% or more, depending on the lender's requirements.

Builder's Risk Insurance

Borrowers are usually required to purchase a builder's risk insurance policy to protect against potential damage during the construction phase.

Our Service Commitment

Get Expert Advice every time from a licensed loan officer with a suite of products to choose from.

Our team strives to deliver excellence. Contact us day or night with any mortgage questions—we’re here when you need us.

Working with us or just thinking of it, we will always be honest and transparent. No sales targets means way better service!

No Hidden Fees: We believe in clear and upfront communication about all costs associated with your mortgage.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Available When & Where

You Want!

Across multiple states, our licensed loan officers will help you from application to funding and beyond.

We work on your schedule. With streamlined technology and dedicated support staffing, your mortgage request is always our priority!

Available When & Where You Want!

Across multiple states, our licensed loan

officers will help you from application to

funding and beyond.

We work on your schedule. With streamlined

technology and dedicated support staffing,

your mortgage request is always our priority!

Book an Appointment

Book an Appointment

See What Our Clients Say About Us!

Meet Our Team

Angle Ogbele

Natasha Staplowski

Darnell Smith

Arlan Zuberi

What is Residential Construction Loans?

A residential construction loan is a short-term financing option designed for individuals or builders in the United States looking to construct a new home or undertake significant renovations on an existing property. Unlike a traditional mortgage that is based on the value of a completed house, a residential construction loan is used to cover the costs of building a home from the ground up or completing major remodeling projects.

How Does a Residential Construction Loan Works ?

Loan Limits: Jumbo loans are for loan amounts that exceed the conforming loan limits, which for most of the U.S. is currently at $647,200 for a single-family home. In high-cost areas, the limit may be higher.

Interest Rates: Jumbo loans often have higher interest rates than conforming loans because they are considered riskier due to the larger amount being borrowed.

Down Payment: Lenders require larger down payments for jumbo loans—often 20% or more of the home's purchase price.

Credit Score: A higher credit score is usually necessary to qualify for a jumbo loan. Lenders may look for a score of 700 or above.

Debt-to-Income Ratio: The debt-to-income ratio (DTI) requirements are usually stricter for jumbo loans. Lenders prefer a DTI below 43%.

Cash Reserves: Lenders may require borrowers to have a certain amount of cash reserves on hand. This could be enough to cover six months or more of mortgage payments.

Documentation: Applicants must provide extensive proof of their financial health, including tax returns, W-2s, 1099s, bank statements, and possibly more, to demonstrate their ability to repay the loan.

Appraisal: A detailed appraisal process is often required to ensure the property's value supports the purchase price and the loan amount.

The residential construction loan allows borrowers to build a home to their specifications and preferences. It is essential to work closely with the lender and builder to ensure that the project stays within budget and on schedule to avoid any complications during the construction phase or when transitioning to permanent financing.

Benefits of Residential Construction Loans

Residential construction loans have several distinct features that differentiate them from traditional home mortgages:

Short-term Financing: Construction loans are short-term loans, with a duration of one year or until the construction of the home is complete.

Interest-Only Payments: During the construction phase, borrowers usually make interest-only payments on the money that has been disbursed to date.

Draw Schedule: Funds are released in a series of draws as construction milestones are completed, rather than a single lump sum at the beginning of the loan.

Variable Rates: The interest rates on construction loans are often variable, which means they can fluctuate with the market during the construction period.

Rigorous Approval Process: Lenders require detailed construction plans, a qualified builder, a detailed budget, and sometimes a down payment.

Builder Approval: The builder or contractor must often be approved by the lender to ensure that they have the necessary qualifications and financial stability to complete the project.

Inspections: The lender will conduct periodic inspections to verify that the construction is progressing as planned before releasing subsequent draws.

Convertibility: Many construction loans are designed to convert to a traditional mortgage after the completion of the home, known as a 'construction-to-permanent' loan.

Down Payment: Borrowers often need to make a significant down payment, which can range from 10% to 20% or more, depending on the lender's requirements.

Builder's Risk Insurance: Borrowers are usually required to purchase a builder's risk insurance policy to protect against potential damage during the construction phase.

These features are designed to manage the risks associated with construction projects and to ensure that the home is completed on time and within budget.

Features of Residential Construction Loans

Applying for a residential construction loan offers several benefits for individuals looking to build a new home:

Customization: It allows you to build a custom home tailored to your specific needs, preferences, and lifestyle, rather than settling for a pre-existing home that may not meet all your requirements.

Control Over Construction: You have more control over the construction process, including the selection of materials, finishes, and fixtures, ensuring the final product is exactly what you want.

Incremental Funding: The loan provides funds in stages as construction progresses, which helps manage cash flow and ensures that builders are paid on time for completed work.

Interest-Only Payments: During the construction phase, you only pay interest on the funds that have been disbursed, not the entire loan amount, which can help keep initial expenses lower.

One-Time Closing: Some construction loans offer a one-time closing, which means you only go through the loan application and closing process once. After construction, the loan automatically converts to a permanent mortgage without the need for a second closing.

Potential Equity Growth: If the construction project is managed well and the final property value exceeds the cost of construction, you may benefit from immediate equity in the new home.

Brand New Home: Upon completion, you'll have a brand-new home that should require less maintenance and fewer repairs in the early years compared to an older home.

Energy Efficiency: New homes can be built with the latest energy-efficient technologies and materials, potentially reducing utility costs and offering a more sustainable living environment.

Overall, a residential construction loan can be an excellent financial product for building your dream home, giving you the financial flexibility to fund the construction process while potentially adding value to your investment from the start.

Quick Links

Other Links

Contact Information

RateShop Mortgage LLC is a licensed mortgage broker in FL and TX.

In accordance with federal law, we do not engage in business practices that discriminate on the basis of race, color, religion, national origin, sex, marital status, or age (provided you have the capacity to enter into a binding contract), nor do we discriminate because any part of your income is derived from public assistance programs, or because you have, in good faith, exercised any right under the Consumer Credit Protection Act. The Federal Trade Commission, Equal Credit Opportunity Division, Washington, DC 20580, is the federal agency responsible for administering these laws.

TEXAS RESIDENTS: CONSUMERS WISHING TO FILE A COMPLAINT AGAINST A MORTGAGE COMPANY OR RESIDENTIAL MORTGAGE LOAN ORIGINATOR LICENSED IN TEXAS SHOULD SEND A COMPLETED COMPLAINT FORM TO THE DEPARTMENT OF SAVINGS AND MORTGAGE LENDING (SML): 2601 N. LAMAR BLVD., SUITE 201, AUSTIN, TEXAS 78705

TEL: 1-877-276-5550. INFORMATION AND FORMS ARE AVAILABLE ON SML'S WEBSITE: SML.TEXAS.GOV.

Copyright 2026. All Rights Reserved Rateshop Mortgage LLC

#1 Voted Mortgage Calculators in Canada

Our Mortgage Experts

Dylan James

Mortgage Agent Level 1

Abdoulaye Sow

Mortgage Agent Level 1

Michael Le Chi

Mortgage Agent Level 1

Heith Gharib

Mortgage Agent Level 1

Sara Fresco

Mortgage Agent level 1