Rental Building

Purchase

Finance Your Rental Property Investment

Competitive financing for multi-family purchases

Loans sized based on property income potential

Potentially lower down payments

888-549-1005

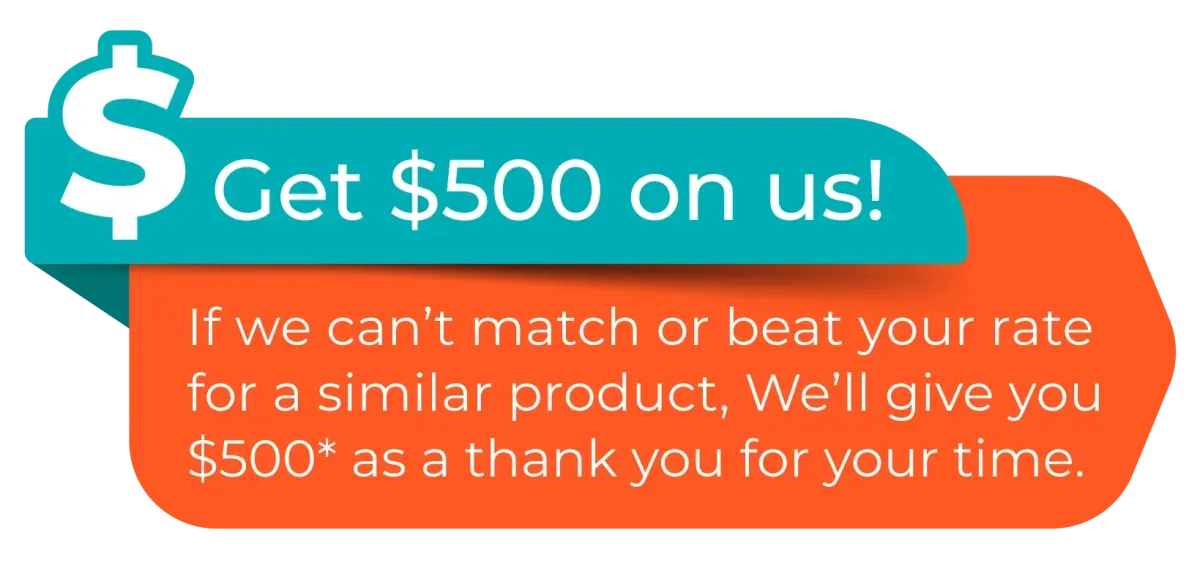

Call for a Free Mortgage Saving Report

No Credit Checks Required

Find Your Perfect Mortgage Match – Let’s Get Started!

FHA Loans

FHA Loans

Or Get a Free Rate Quote

1800-725-9946

Make your dream of owning a home a reality.

Low down payment options

Flexible credit requirements

Competitive interest rates we shop for you

888-549-1005

Call for a Free Mortgage Saving Report

No Credit Checks Required

Rental Building

Purchase

Or Get a Free Rate Quote

1800-725-9946

Finance Your Rental Property Investment

Competitive financing for multi-family purchases

Loans sized based on property income potential

Competitive interest rates we shop for you

888-549-1005

Call for a Free Mortgage Saving Report

No Credit Checks Required

Secure Financing for Your Rental Property Purchase — Fast Approvals, Great Rates, and Maximum Cash Flow!

Flexible Financing for Multi-Unit and Rental Properties: — Ideal for growing your real estate portfolio.

No Personal Income Verification Options Available: — Qualify based on rental income potential.

Competitive Interest Rates: — We secure the best rates to help maximize your monthly cash flow.

Fast Pre-Approval Process: — Move quickly on lucrative rental property deals without missing opportunities.

Tailored Loan Programs for Investors: — Choose terms that fit your investment strategy and long-term goals.

Low Closing Costs & Transparent Terms: — Keep more of your profits with no hidden fees or surprises.

Find Your Perfect Mortgage Match – Let’s Get Started!

Start with our Mortgage Approval Tool!

Start with our Mortgage Approval Tool!

Start with our Mortgage Approval Tool!

Home Purchase

Ready to buy? Get pre-approved in minutes and secure competitive rates tailored to your budget. Whether you’re a first-time buyer or upgrading, we’ll help you close faster.

Home Refinance

Slash your monthly payments or tap into your equity with flexible refinancing options. Rate-and-term, cash-out, or FHA streamline—we’ve got your best deal.

Home Equity

Need funds for renovations, debt consolidation, or emergencies? Access up to 90% of your home’s value with low rates and tax-deductible interest

Reverse

Age 62+? Keep ownership, stay in your home, and access tax-free cash. No monthly payments required—ever. FHA-insured and risk-free.

Our Service Commitment

No Hidden Fees: We believe in clear and upfront communication about all costs associated with your mortgage.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Get Expert Advise, every time from a licensed loan officer with a suite of products to choose from.

Our Team strives to deliver excellence, reach us day or night about any of your mortgage questions, we’re here for you when you need.

Working with us or just thinking of it, we will always be honest and transparent. No sales targets means way better service!

Largest Lender Network in Florida, Georgia & Texas

What Are Rental Building Purchase Loans?

A rental building purchase loan is a specialized financing solution for investors seeking to acquire residential or commercial properties—ranging from single-family homes and multifamily units to apartment buildings and commercial spaces—that generate consistent rental income. These loans enable investors to expand their real estate portfolios and increase passive income through attractive rental yields. By carefully evaluating associated costs, potential returns, and inherent risks, investors can strategically use rental building purchase loans to secure valuable assets and achieve long-term financial growth in the competitive real estate market.

How Does a Rental Building Purchase Loans Works?

Approval Process

In a rental building purchase, the approval process is crucial. Borrowers must submit comprehensive construction plans, a detailed budget, and a realistic timeline for the project. Lenders assess these documents alongside the borrower's creditworthiness and project feasibility to ensure the investment is sound and aligns with market standards.

Loan Disbursement

Unlike traditional home loans that offer a lump sum for existing properties, construction loans for rental building purchases provide funds in stages, known as draws. Each draw is released as the project reaches predefined milestones, ensuring that financing is closely tied to construction progress and helping keep the project on track.

Interest-Only Payments

During the construction phase, borrowers typically make interest-only payments on the disbursed amounts. This means that as additional funds are drawn to finance different stages of the project, the interest payments may increase, reflecting the incremental use of funds throughout the construction process.

Construction Phase

The construction phase generally spans around 12 months, during which the rental building must be completed within the established timeline and quality standards. Lenders often conduct inspections at various stages to verify that the project meets the agreed-upon specifications before releasing subsequent draws.

Conversion to Permanent Financing

Once construction is complete, the loan transitions to permanent financing. This conversion can occur as a construction-to-permanent loan—where the initial loan seamlessly converts into a long-term mortgage—or as two separate loans, with a new mortgage paying off the construction loan based on the property's final appraised value.

End Loan

If the construction financing is provided as a separate loan, borrowers must apply for an end loan upon project completion. The end loan is calculated based on the finished value of the rental property, effectively converting the construction loan into a standard, permanent mortgage that facilitates long-term ownership and rental income generation.

Features of Rental Building Purchase Loans

Leverage

A loan allows you to purchase a larger property than you might otherwise afford with cash, increasing your potential investment returns.

Cash Flow Management

By financing a property, you can maintain liquidity and have cash on hand for other investments or expenses.

Tax Deductions

The interest paid on a residential building purchase loan may be tax-deductible, reducing the overall cost of borrowing.

Asset Appreciation

If the property value increases over time, you can benefit from the appreciation while having used the bank's money to finance the majority of the purchase.

Fixed Payments

With a fixed-rate loan, your mortgage payments remain consistent over time, making it easier to budget and plan for property expenses.

Rental Income

The property can generate ongoing rental income, which can be used to pay the mortgage and other property-related expenses, potentially providing a steady income stream.

Building Equity

The property can generate ongoing rental income, which can be used to pay the mortgage and other property-related expenses, potentially providing a steady income stream.

Diversification

Investing in real estate can diversify your investment portfolio, which can be a hedge against inflation and market volatility.

Long-Term Financial Planning

Owning a residential building can be part of a long-term financial strategy, contributing to wealth accumulation and retirement planning.

Control Over Property

As the property owner, you have control over property management decisions, tenant selection, and property improvements to increase value.

Benefits of Rental Building Purchase Loans

Loan Purpose

Specifically designed to finance the purchase of residential properties such as single-family homes, condominiums, townhouses, and multi-family units.

Down Payment

Generally requires a down payment ranging from 20-30% of the property's purchase price, though this can vary based on the lender and the borrower's creditworthiness.

Loan Terms

The length of the loan can vary, with common terms being 15, 20, or 30 years. Some lenders may offer adjustable-rate mortgages (ARMs) or fixed-rate mortgages (FRMs).

Interest Rates

The interest rates can be either fixed, meaning they stay the same throughout the term of the loan, or adjustable, meaning they can change at specified times.

Amortization

Loans are amortized, meaning payments are spread out over the life of the loan, with early payments going more towards interest and later payments going more towards principal.

Closing Costs

Borrowers are responsible for closing costs, which can include loan origination fees, appraisal fees, title searches, title insurance, and other associated costs.

Debt Service Coverage Ratio (DSCR)

Lenders often require that the property's income is sufficient to cover the mortgage payments and other expenses, measured by the DSCR.

Prepayment Penalties

Some loans may include prepayment penalties, which are fees charged if the borrower pays off the loan early.

Due Diligence Requirements

Lenders will require an appraisal of the property, an inspection, and a review of the financials, including income and expense statements, to ensure the property is a sound investment.

Insurance Requirements

Borrowers will need to secure property insurance and, depending on the location, may also need additional coverage such as flood insurance.

Credit and Income Verification

Borrowers must provide proof of income, employment, and a good credit history to qualify for the loan.

Property Use

The property must be used for residential purposes, and the terms of the loan may vary depending on whether it's owner-occupied or an investment property.

Our Service Commitment

Get Expert Advice every time from a licensed loan officer with a suite of products to choose from.

Our team strives to deliver excellence. Contact us day or night with any mortgage questions—we’re here when you need us.

Working with us or just thinking of it, we will always be honest and transparent. No sales targets means way better service!

No Hidden Fees: We believe in clear and upfront communication about all costs associated with your mortgage.

Tailored Solutions: Our advisors work closely with you to find mortgage solutions that are customized to your financial situation.

Available When & Where

You Want!

Across multiple states, our licensed loan officers will help you from application to funding and beyond.

We work on your schedule. With streamlined technology and dedicated support staffing, your mortgage request is always our priority!

Available When & Where You Want!

Across multiple states our Licensed Loan officers will help you from the application to the funding and beyond. We workon your schedule, with streamlined technology and support staffing, your mortgage request will always be a priority!

Book an Appointment

Book an Appointment

See What Our Clients Say About Us!

Meet Our Team

Angle Ogbele

Natasha Staplowski

Darnell Smith

Arlan Zuberi

What is Rental Building Purchase?

A rental building purchase loan is a type of financing used by investors to purchase residential or commercial properties that will be rented out to tenants. These loans can be used for various types of rental properties, including single-family homes, multifamily units, apartment buildings, and commercial spaces.

Investors use rental building purchase loans to expand their real estate portfolios and increase passive income through rental yields. It is important for investors to carefully evaluate the costs, potential returns, and risks associated with owning rental properties before securing such a loan.

How Does a Rental Building Purchase Works ?

Approval Process: Before a loan is granted, the borrower must provide the lender with a comprehensive set of construction plans, a realistic budget, and a timeline for the project. The lender will also assess the borrower's creditworthiness and the feasibility of the project.

Loan Disbursement: Unlike traditional home loans, which provide a lump sum to purchase an existing property, construction loans provide funds in stages as the building progresses. These stages are often referred to as 'draws.' Each draw is released after certain milestones are completed in the construction process.

Interest-Only Payments: During the construction phase, borrowers pay interest only on the amount of money that has been disbursed. This means that as the project progresses and more draws occur, the interest payment can increase.

Construction Phase: The construction phase usually has a timeline (often 12 months) during which the construction must be completed. The lender may require inspections before releasing subsequent draws to ensure that the project meets the agreed-upon standards and is on schedule.

Conversion to Permanent Financing: Once the construction is complete, the construction loan converts to a permanent mortgage. This conversion can be structured as a 'construction-to-permanent' loan, where the loan is in place from the start of construction through the life of the mortgage, or as two separate loans: a construction loan followed by a new mortgage to pay off the construction loan.

End Loan: If the construction loan is separate from the mortgage, upon completion of the building, the borrower must apply for an 'end loan' to pay off the construction loan. The end loan is based on the finished value of the home and converts the construction loan into a standard mortgage.

It's worth noting that the specifics of a rental building purchase loan can vary based on the lender's policies, the type of property, and the borrower's financial situation.

Benefits of Rental Building Purchase

Here are the features of a Residential Building Purchase Loan:

Loan Purpose: Specifically designed to finance the purchase of residential properties such as single-family homes, condominiums, townhouses, and multi-family units.

Down Payment: Generally requires a down payment ranging from 20-30% of the property's purchase price, though this can vary based on the lender and the borrower's creditworthiness.

Loan Terms: The length of the loan can vary, with common terms being 15, 20, or 30 years. Some lenders may offer adjustable-rate mortgages (ARMs) or fixed-rate mortgages (FRMs).

Interest Rates: The interest rates can be either fixed, meaning they stay the same throughout the term of the loan, or adjustable, meaning they can change at specified times.

Amortization: Loans are amortized, meaning payments are spread out over the life of the loan, with early payments going more towards interest and later payments going more towards principal.

Closing Costs: Borrowers are responsible for closing costs, which can include loan origination fees, appraisal fees, title searches, title insurance, and other associated costs.

Debt Service Coverage Ratio (DSCR): Lenders often require that the property's income is sufficient to cover the mortgage payments and other expenses, measured by the DSCR.

Prepayment Penalties: Some loans may include prepayment penalties, which are fees charged if the borrower pays off the loan early.

Due Diligence Requirements: Lenders will require an appraisal of the property, an inspection, and a review of the financials, including income and expense statements, to ensure the property is a sound investment.

Insurance Requirements: Borrowers will need to secure property insurance and, depending on the location, may also need additional coverage such as flood insurance.

Credit and Income Verification: Borrowers must provide proof of income, employment, and a good credit history to qualify for the loan.

Property Use: The property must be used for residential purposes, and the terms of the loan may vary depending on whether it's owner-occupied or an investment property.

Features of Rental Building Purchase

Applying for a residential building purchase loan offers several benefits for investors and property owners:

Leverage: A loan allows you to purchase a larger property than you might otherwise afford with cash, increasing your potential investment returns.

Cash Flow Management: By financing a property, you can maintain liquidity and have cash on hand for other investments or expenses.

Tax Deductions: The interest paid on a residential building purchase loan may be tax-deductible, reducing the overall cost of borrowing.

Asset Appreciation: If the property value increases over time, you can benefit from the appreciation while having used the bank's money to finance the majority of the purchase.

Fixed Payments: With a fixed-rate loan, your mortgage payments remain consistent over time, making it easier to budget and plan for property expenses.

Building Equity: As you make loan payments, you build equity in the property, which can be leveraged for future investments or used as collateral.

Rental Income: The property can generate ongoing rental income, which can be used to pay the mortgage and other property-related expenses, potentially providing a steady income stream.

Diversification: Investing in real estate can diversify your investment portfolio, which can be a hedge against inflation and market volatility.

Long-Term Financial Planning: Owning a residential building can be part of a long-term financial strategy, contributing to wealth accumulation and retirement planning.

Control Over Property: As the property owner, you have control over property management decisions, tenant selection, and property improvements to increase value.

These benefits make residential building purchase loans an attractive option for individuals looking to invest in real estate. However, it's important to carefully consider the risks and responsibilities associated with being a property owner and landlord before taking out a loan.

Quick Links

Other Links

Contact Information

RateShop Mortgage LLC is a licensed mortgage broker in FL and TX.

In accordance with federal law, we do not engage in business practices that discriminate on the basis of race, color, religion, national origin, sex, marital status, or age (provided you have the capacity to enter into a binding contract), nor do we discriminate because any part of your income is derived from public assistance programs, or because you have, in good faith, exercised any right under the Consumer Credit Protection Act. The Federal Trade Commission, Equal Credit Opportunity Division, Washington, DC 20580, is the federal agency responsible for administering these laws.

TEXAS RESIDENTS: CONSUMERS WISHING TO FILE A COMPLAINT AGAINST A MORTGAGE COMPANY OR RESIDENTIAL MORTGAGE LOAN ORIGINATOR LICENSED IN TEXAS SHOULD SEND A COMPLETED COMPLAINT FORM TO THE DEPARTMENT OF SAVINGS AND MORTGAGE LENDING (SML): 2601 N. LAMAR BLVD., SUITE 201, AUSTIN, TEXAS 78705

TEL: 1-877-276-5550. INFORMATION AND FORMS ARE AVAILABLE ON SML'S WEBSITE: SML.TEXAS.GOV.

Copyright 2026. All Rights Reserved Rateshop Mortgage LLC

#1 Voted Mortgage Calculators in Canada

Our Mortgage Experts

Dylan James

Mortgage Agent Level 1

Abdoulaye Sow

Mortgage Agent Level 1

Michael Le Chi

Mortgage Agent Level 1

Heith Gharib

Mortgage Agent Level 1

Sara Fresco

Mortgage Agent level 1